$FCX: Freeport-McMoRan - The Pure Play on Copper’s Coming Decade

Why the world’s largest copper miner is positioned to capture the full upside of a structural shortage

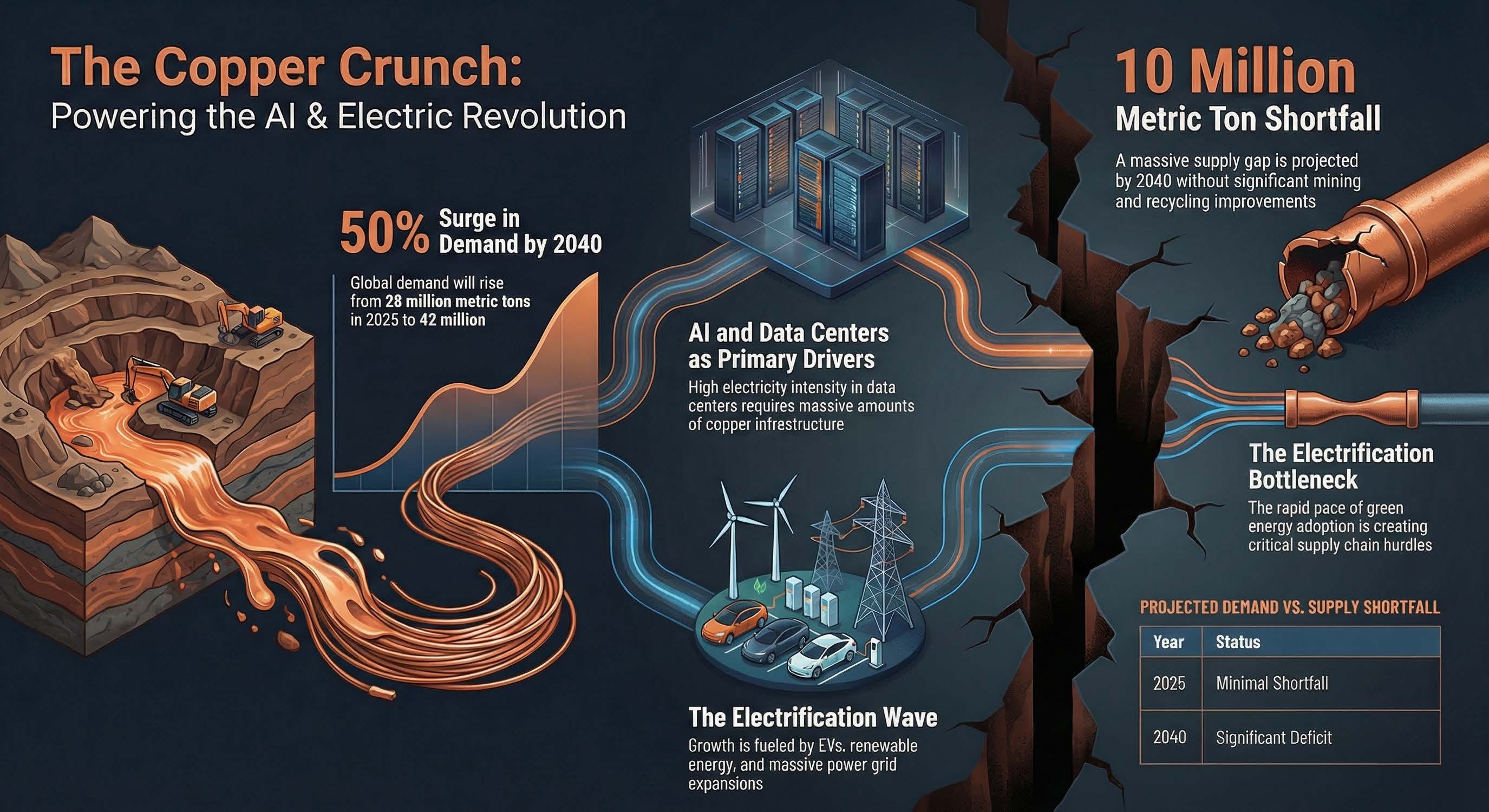

Copper is essential to modern electrification due to its superior electrical conductivity, which has no viable substitute at scale. The metal is critical across every major infrastructure category: power transmission and distribution networks, electric motors, transformers, renewable energy systems, and data centers. A single wind turbine contains sever…